Let’s Meet, on Your Terms

No pressure, no obligations — just an open conversation about your goals.

Tax rates are high, and they are likely going higher. Wealthy families and those in higher tax brackets are looking to their advisors to help lower their tax burden. One strategy that is gaining popularity is Private Placement Life Insurance (“PPLI”). When properly structured, these policies can be a powerful tool for high-net-worth families providing four key benefits that I will outline in this paper.

- Investment Flexibility

- Tax Mitigation and Increased Wealth Creation

- Asset Protection

- Wealth Transfer

Eligibility

First, let’s talk about who should consider this strategy as PPLI policies are not for everyone. Policy owners must be accredited investors or qualified purchasers. Furthermore, owners should have the ability to fund $1 million or more in annual premiums for several years, typically $3-$5 million, though many investors are allocating over $10 million to this strategy. Because of this, a good candidate for PPLI starts with investors in the $20-$25 million net worth range.

Investment Flexibility

Traditional insurance policies offer limited investment options to their policy holders, typically mutual funds or investment products approved by the insurance carrier. Until recently, PPLI policies only allowed investments in Insurance Dedicated Funds, of which there were only a few players in the space. Recently, with the signing of H.R. 133 being signed into law investment options have expanded to allow for Separately Managed Accounts with investment advisors such as Simon Quick[1]. This allows the investment advisor to allocate to essentially anything they typically recommend in traditional portfolios.

Assets held within PPLI policies can maintain access to all investment choices and asset classes. To maximize the benefit of the elimination of taxes, it’s best to invest in tax-inefficient investments. This includes private partnership vehicles such as hedge funds, private equity, venture capital and private credit.

The primary investment limitation of assets invested in PPLI relates to the investor control doctrine. This limits the amount of direction the policy owner or insured can exert over the investment decisions. While free to choose the investment advisor and discuss asset class exposure, the policyowner may not have control over specific investment selections. The policyholder can choose an advisor and give direction around asset class exposure and risk tolerance, but the advisor must be free to choose the specific investments. It is important to work with experienced professionals to ensure the strategy is executed correctly.

Tax Mitigation and Increased Wealth Creation

Part of what makes PPLI such a compelling vehicle for investors is that the assets grow tax free, similar to a Roth IRA but without the limitations on how much you can contribute. When it comes time to withdraw assets, you can do so tax free. This is what makes PPLI so powerful, it doubles the benefit since you are not only growing assets tax free but also withdrawing assets tax free.

Let’s explore an example of what tax-free growth might look like. The capital gains tax is a tax you pay on the profit earned from selling assets. If you have taxable assets invested with a hedge fund manager who actively trades in the strategy, you will be paying a capital gains tax each time a share is sold. If you are in a high-income bracket, those taxes can really compound.

While a PPLI contract can have nearly any investment in the policy, placing your highly tax-inefficient investments into a PPLI policy can be an effective way to take advantage of those investment strategies while mitigating their tax impact.

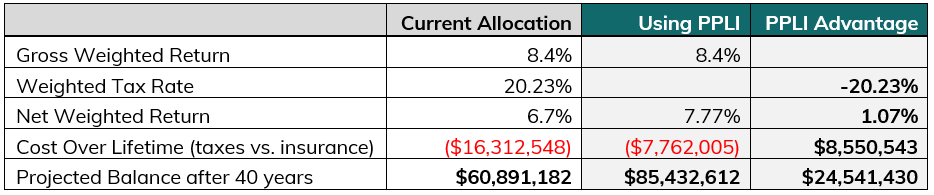

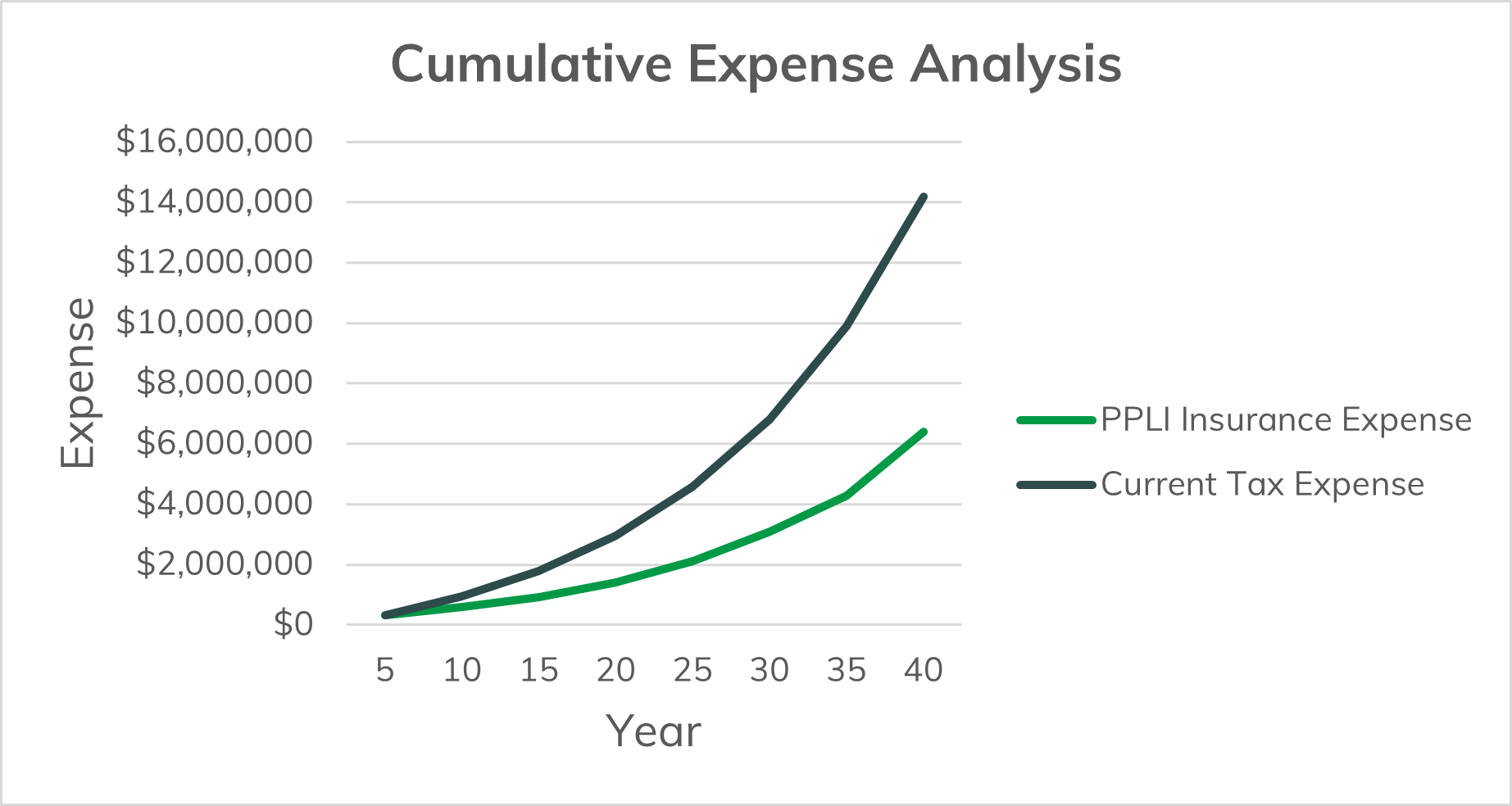

There are insurance costs associated with the strategy, but by paying insurance costs instead of income tax on the portfolio earnings, a higher net rate of return is achieved.

Example: Keeping the investment allocation the same, the case study below details an initial investment of $5 million in a brokerage account compared to $5 million in a PPLI product over the client’s lifetime (a 40-year time horizon). The client resides in NJ and has a moderately aggressive risk tolerance. As such, the gross weighted return of the portfolio is 8.4%.

Asset Protection

Another key benefit to PPLI is that it can protect your assets from creditors. To understand how a PPLI policy can provide asset protection, let’s first consider the asset protection benefits of life insurance policies more broadly. Because life insurance is considered essential for the policy owner’s beneficiaries to maintain a minimum level of financial well-being, they provide a greater level of protection from the claims of creditors than other asset classes might[2]. This varies by state, but PPLI can enhance creditor protection in comparison to owning an investment outright.

Wealth Transfer

As with any life insurance policy, the death benefit is the money paid to your beneficiaries either as a lump sum, or installments, after your death[3]. While these funds pass income tax free to your beneficiaries, the proceeds may be subject to federal estate tax. Placing PPLI within certain trust structures enables the death benefit to pass to the beneficiaries free of wealth transfer taxes. Thus, when everything aligns, investors can both grow their assets income tax-free and pass them on estate tax-free.

Fees and Other Considerations

While PPLI is technically a life insurance policy, it is designed very differently than traditional life insurance policies. The policies are structured in such a way that they provide the least amount of life insurance legally allowed by the IRS. This is done in order to minimize the expenses and fees of the product. Traditional life insurance has opacity surrounding expenses and fees. Recent developments in the PPLI marketplace have improved transparency while minimizing complexity and policy costs. A reputable PPLI professional will disclose all costs, fees and expenses up front.

If the policy is structured as non-MEC (which is easy to do), funds may be withdrawn tax-free for any reason from the policy cash value. This is the amount managed by the advisor and is subject to the liquidity of the underlying funds.

Private Placement Variable Annuities (“PPVA”) are also available. However, these have less favorable tax benefits when compared to PPLI since withdrawals taken from an annuity are first taxed as ordinary income. They also come along with a 10% penalty if withdrawals are made before the age of 59 ½. At death of the owner, any amounts paid are taxed as ordinary income. PPVA can still make sense for some, especially those that don’t anticipate the need for withdrawals, as returns can compound tax-free annually.

Conclusion

The recent tax law changes, coupled with the increasing number of available investment options, make for a particularly interesting time to explore PPLI as a tax-efficient investment solution. Your Simon Quick Advisor is available to talk to you about whether PPLI is worth considering as part of your overall financial plan.

REFERENCES

[2] https://www.mosessinger.com/uploads/Asset_Protection_Riches_Out_of_Reach.pdf

[3] https://www.guardianlife.com/life-insurance/death-benefits

DISCLAIMER

Simon Quick Advisors, LLC (Simon Quick) is an SEC registered investment adviser with a principal place of business in Morristown, NJ. Simon Quick may only transact business in states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. A copy of our written disclosure brochure discussing our advisory services and fees is available upon request. References to Simon Quick as being “registered” does not imply a certain level of education or expertise. No information provided shall constitute, or be construed as, an offer to sell or a solicitation of an offer to acquire any security, investment product or service, nor shall any such security, product or service be offered or sold in any jurisdiction where such an offer or solicitation is prohibited by law or registration. Additionally, no information provided in this report is intended to constitute legal, tax, accounting, securities, or investment advice nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type. Past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. It should not be assumed that future performance of any specific investment or investment strategy will be profitable, equal any corresponding indicated performance level(s), be suitable for your portfolio or individual situation, or prove successful.

Investing in Alternative Investments may not be suitable for all investors and involves a high degree of risk. Many Alternative Investments are highly illiquid, meaning that you may not be able to sell your investment when you wish.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product will be profitable, equal any corresponding indicated historical performance level(s), be suitable for a portfolio or individual situation, or prove successful. This document is strictly confidential and may not be reproduced or distributed in whole or in part without the prior written consent of Simon Quick Advisors. This presentation represents proprietary information that may not be shared without express permission from Simon Quick Advisors.

This information is being provided to you on a confidential basis. By accessing and reviewing this document, you acknowledge and agree that (i) you will not disclose or distribute this information, in whole or in part, to any third party without the prior written consent of the investment manager, Simon Quick Advisors and (ii) that such information is being provided to you for informational purposes only as a current or potential investor qualified to invest in hedge funds and other alternative investments. It does not constitute an offer to sell or a solicitation of an offer to buy any securities. Any such offer of solicitation will be made only by means of a formal Offering Memorandum that will be furnished to prospective investors.

This material is for intended to be for general and educational purposes only and is being furnished on a confidential basis to the recipient for discussion purposes only. You should not make any decision, financial, investment, trading or otherwise, based on any of the information contained herein without undertaking independent due diligence and consultation with a professional advisor of his/her choosing. You understand that you are using any and all information herein at your own risk. No information provided herein shall constitute, or be construed as an offer or recommendation to sell, acquire, or hold any security, investment product or service, nor shall any such security, product or service be offered or sold in any jurisdiction where such an offer or solicitation is prohibited by law or registration.

Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Simon Quick Advisors is neither a law firm nor a certified public accounting firm and no portion of this document’s content should be construed as legal or accounting advice.

This report includes forward-looking statements. All statements that are not historical facts are forward-looking statements, including any statements that relate to future market conditions, results, operations, strategies or other future conditions or developments and any statements regarding objectives, opportunities, positioning or prospects. Forward-looking statements are necessarily based upon speculation, expectations, estimates and assumptions that are inherently unreliable and subject to significant business, economic and competitive uncertainties and contingencies. Forward-looking statements are not a promise or guaranty about future events.

Information herein has been obtained from third party sources. While we believe the source to be accurate and reliable, Simon Quick Advisors Simon has not independently verified the accuracy of information. In addition, Simon Quick Advisors makes no representations or warranties with respect to the accuracy, reliability, or utility of information obtained from third parties.

Simon Quick Advisors, LLC (Simon Quick) is an SEC registered investment adviser with a principal place of business in Morristown, NJ. Simon Quick may only transact business in states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. A copy of our written disclosure brochure discussing our advisory services and fees is available upon request. References to Simon Quick Advisors as being “registered” does not imply a certain level of education or expertise.