Let’s Meet, on Your Terms

No pressure, no obligations — just an open conversation about your goals.

Investors over the past year have faced levels of economic uncertainty and market volatility that haven’t been seen in years. The S&P 500 index was down nearly 20% in 2022. Moreover, the index recorded 46 moves of 2% in both directions throughout the year, which is the choppiest performance the index has seen since 2009 – roughly four times the 10-year average.

Emotions often run high during times like this. After all, watching your portfolio drop drastically for days or even weeks can be distressing. Unfortunately, these feelings can sometimes lead investors to make emotional decisions that aren’t in their best interest.

The Behavior Gap

The Behavior Gap, published in 2012, coined the phrase ‘the behavior gap’ to describe the impact of human decisions on investment returns.[1] The book states that human beings are hard wired to avoid pain and seek pleasure and security. So, from an investing standpoint, it feels natural to sell securities when everyone else is spooked and buy securities when everyone else is giddy. While this might feel right, it often leads to underperformance over the long term.

The relatively new but growing field of behavioral finance suggests there are predictable ways that investors tend to act irrationally. Financial and investment decision-making is sometimes influenced as much by human psychology as it is by quantifiable data.

Each year, investment research firm Dalbar, Inc. publishes a Quantitative Analysis of Investor Behavior Report that studies investor performance in mutual funds. This report demonstrates that, more often than not, people are their own worst enemies when it comes to investing their money. More specifically, people often succumb to short-term strategies based on emotion, like market timing or chasing performance, instead of being disciplined and sticking to their long-term plan.

Unfortunately, this tends to lower long-term investment returns. According to the most recent Dalbar report, the average equity fund investor realized a 7.13% return over the 30-year period between January 1, 1992, and December 31, 2021. However, the S&P 500 notched a 10.65% return over this period. The result is a behavior gap of more than 3.5%. On a $100,000 investment, this behavior gap would cost the average investor nearly $1.3 million.[2]

Managing Human Emotions

The key to avoiding the behavior gap is learning how to manage the emotions that can lead to short-term investing decisions that diminish long-term returns. This is one of the main things we focus on here at Simon Quick. When discussing the tenets of behavioral finance with our clients, we focus on:

- Traditional theories and principals of finance.

- Psychology, or understanding how human behavior affects investing.

- Neuroscience or physiology, or in other words, how people are hard-wired to respond to situations.

Part of our process in constructing portfolios and running projections incorporates the unknown — because there are always unknowns, both in the financial markets and in life. Nobody knows when extreme market volatility is going to occur. Unfortunately, it can sometimes occur at the worst possible time, like when you’re ready to retire.

While there are trends when it comes to market movements, these trends are unpredictable and can move in unexpected directions. There’s a reason why investment prospectuses always say, “Past performance is not indicative of future returns.” In the same way, life events and worst-case scenarios can also be hard to predict. This includes our health and, ultimately, the length of our life.

In fact, the only thing that’s truly certain is that surprises will occur! This is why it’s so important to plan ahead for the unexpected and know what you’ll do when life throws you a curveball.

The Alignment Model

Each person has his or her own emotions and morals. But there’s a difference between emotional and moral intelligence and emotional and moral competence.

- Emotional and moral intelligence is knowing what our emotions and morals are. Or in other words, recognizing what you are feeling in the moment and being able to differentiate between your emotions and how universal moral principles and values apply to your personal goals and actions.

- Emotional and moral competence is the ability to manage your emotions and act on your moral principles, even when you have competing emotions.

We each have our own moral compass, which is our ideal self and incorporates our values and intentions. Then we have our actual behavior, or our real self, which is where we work to align our thoughts, feelings, and actions. The objective is to define our goals by aligning our behavior and emotions with our intentions and values.

It’s important to understand your values and discuss them with your financial advisor, so he or she is also aware of them. You then want to make sure you’re setting goals that are in alignment with your values and that the actions you take are in support of these goals and values.

For instance, it might not make sense to set up a charitable foundation if helping others isn’t one of your top values. However, this might be a “nice to have” after other values have been satisfied first, such as buying a vacation home to align with the value of spending time with family.

The Impact of Physiology on Decision Making

It’s important to realize that physiological reactions can prevent us from thinking logically or coherently. This can be caused by the amygdala, which is in the limbic system of the brain and is known for causing the “fight or flight” response.

The amygdala sends an impulse to the liver that produces a stress hormone called cortisol when there is a threat. The body then makes preparations to our extremities, including the prefrontal cortex, which is the logical part of the brain. In other words, we’re hard wired to be emotional first and logical second.

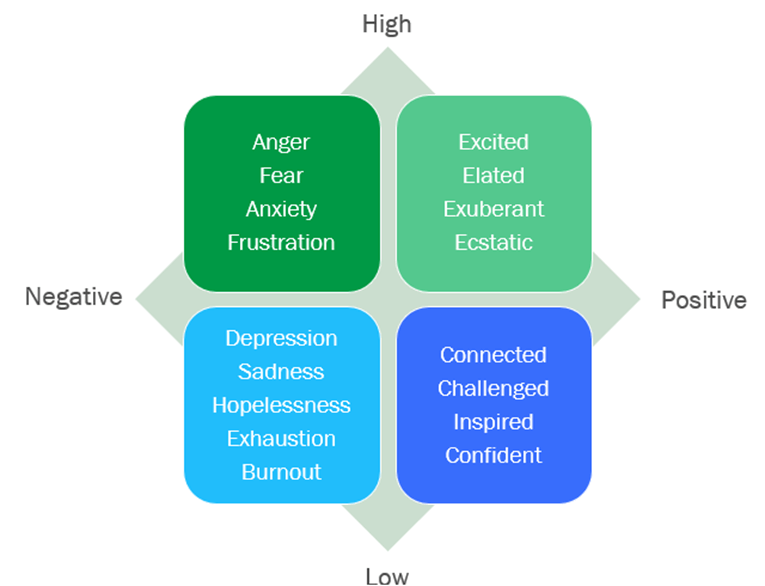

Overly positive emotions can be just as detrimental as overly negative ones. Low-energy, negative emotions (represented in the lower left quadrant in the graphic below) are caused by prolonged periods of stress and mental anguish. High-energy, negative emotions (upper left quadrant) are caused by negative stressors that prevent clear and thoughtful decisions.

High energy, positive emotions (upper right quadrant) can also hurt decision making. An example might be if you have a large liquidity event (like an inheritance) and decide to buy an extravagant home that still may be beyond your means.

Most people make their best decisions somewhere between the high and low energy quadrants when they’re in a positive emotional state. The energy level needs to be high enough to be motivating but not so high that it creates irrational exuberance.

Consider the Four R’s

These four R’s can help you limit the potentially negative impact of physiology on your investment decision making:

- Recognize your thoughts and emotions. Ask yourself, “How am I feeling? What am I thinking?”

- Reflect on any biases, values or principles as they relate to the big picture and your long-term goals. Ask yourself, “Have my goals or values changed?”

- Reframe your self-talk and account for biases to avoid emotional responses. Ask yourself, “What are other options, and what are the trade-offs?”

- Respond with a decision that’s consistent with your principles, values, and goals. Ask yourself, “What is the best choice right now?”

All of this ties back to navigating your financial plan and investment portfolio. At Simon Quick Advisors, we feel strongly about working with your Client Advisory team to develop an overall financial plan that limits the potential impact of emotional decision making. We try to focus clients on all aspects of their financial life, including:

- Retirement lifestyle

- Cash flow needs

- Desires to leave a legacy

- Charitable intent

- Tax, estate and insurance planning

Uncertainty … is Certain

There’s no way to eliminate the certainty of uncertainty. We know volatile markets will occur — we just don’t know when, for how long and to what extent. So, we create financial plans and projections to account for this unknown volatility.

When volatility and market downturns occur, it’s important to remember that you planned for this, and it won’t last forever. At this time, you will likely be in one of the negative emotional quadrants (either high or low energy), which is not a good time to be making financial and investment decisions. If you do make decisions during this time, be sure to utilize the four R’s listed above.

We would be happy to answer any questions you have about behavioral finance and removing emotions from financial and investing decisions. Feel free to call us at (973) 525-1000 or send an email to [email protected].

References

- Richards, Carl ‘The Behavior Gap’ Penguin Group, New York, 2012

- Coleman, Murray ‘Dalbar QAIB 2022: Investors are Still Their Own Worst Enemies,’ Index Fund Advisors, 2017

DISCLAIMER

Simon Quick Advisors, LLC (Simon Quick) is an SEC registered investment adviser with a principal place of business in Morristown, NJ. Simon Quick may only transact business in states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. A copy of our written disclosure brochure discussing our advisory services and fees is available upon request. References to Simon Quick as being “registered” does not imply a certain level of education or expertise. No information provided shall constitute, or be construed as, an offer to sell or a solicitation of an offer to acquire any security, investment product or service, nor shall any such security, product or service be offered or sold in any jurisdiction where such an offer or solicitation is prohibited by law or registration. Additionally, no information provided in this report is intended to constitute legal, tax, accounting, securities, or investment advice nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type. Past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. It should not be assumed that future performance of any specific investment or investment strategy will be profitable, equal any corresponding indicated performance level(s), be suitable for your portfolio or individual situation, or prove successful.