Onward and Upward

The price per barrel of oil fell from $60 to a NEGATIVE $35 in a matter of months last year. More than 4% of California burned during the summer wildfires, the most of any season in history. Social unrest led to tens of millions of people protesting across the country for months. A record 159 million Americans voted in the November elections, flipping both the White House and Senate to the Democrats. Former Chairperson of the Federal Reserve, Janet Yellen, was nominated Secretary of Treasury, to be only the second person ever to serve in both roles. Murder hornets have infiltrated the country. Each of these events are individually significant, but none have had a larger human and economic impact as the COVID pandemic. Today, vaccines are rolling out and movie theaters are re-opening, but the pandemic has left a sociological imprint that has changed the way we engage on a personal, professional, and hygienic level. Virtual learning and meetings are part of the norm and have improved productivity. Online shopping and grocery delivery has been adopted by even the most reluctant baby boomers. Multi-monitor workstations are now fixtures in our homes and closets are stocked with backup toilet paper.

Capital markets have adapted as well. While the March 2020 sell-off was dramatic, the recovery was rational, if not a bit accelerated. As sharp as the decline was, investors quickly and confidently gobbled up assets trading at bargain basement prices in a matter of weeks, not months. By the second half of the year, stocks and bonds were well off their lows and were trading higher on the optimism of improving economic fundamentals and vaccine trials. As the fog lifted from the November elections, indices were setting new all-time highs, and the riskier the asset, the better the return.

We moved to an overweight recommendation in stocks at the beginning of the year. We recognize that this is not necessarily a contrarian view as much of Wall Street also is positioned that way, however we cannot ignore the improved economic environment we are in. Fiscal and monetary policy is highly accommodative to risk assets as stimulus is supportive to a recovery and low rates are pushing investors into stocks to generate returns. Vaccine roll-outs and better visibility into Washington DC policy and the Fed’s dovishness have cut off a lot of the left-tail risks to markets. We do expect episodic volatility but think the economic bear case scenario has been curtailed and there is a clear path to recovery and growth over the next couple years. Where we are more nuanced in our view is in our expectations for small- and mid-cap stocks to outpace more defensive large caps, and international markets are finally rallying, supported by strong growth, relatively cheaper valuations, and a weakening US Dollar. While passive investing has been in the limelight for a while now, we believe that higher valuations and greater stock dispersion should benefit long-only and long-short equity managers in finding opportunities for excess return in 2021.

Source: JPMorgan

We maintain an underweight recommendation in fixed income as low absolute yields and heightened inflationary risks weigh on the asset class. While Treasuries can provide nominal capital preservation and possibly dampen equity volatility, there is not a compelling REAL return opportunity in traditional bonds for the foreseeable future.

Economies are Recovering

The COVID recession was significant in its global reach and severity, impacting almost every country in the world and exceeding the depths experienced in 2009. The suddenness of city shutdowns and travel restrictions sent the economy into freefall in the second quarter of 2020. The sudden downward shock was countered with an aggressive response as the Fed and Treasury brushed off the 2008 playbook of quantitative easing and fiscal stimulus as to pull the economy out of recession. By stabilizing the capital markets, and putting money into people’s hands, the government was able to stave off a potential depression. While there are still significant economic challenges and long-term balance sheet ramifications that need to be addressed, it is now expected that many of the major countries will emerge at an above-normal growth trend over the next few years. Specific to the US, the economy is expected to grow at an above-average pace of 4.9% and 3.6% for the next two years. This is in comparison to the 2-3% range we had achieved since 2009.

Source: Goldman Sachs

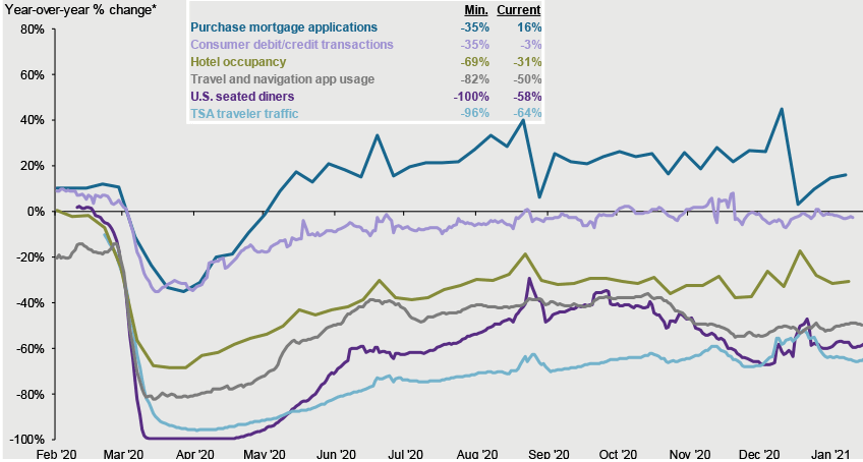

Both the lowest and highest unemployment rates the country has ever experienced in the last 50 years occurred in 2020 and were just two months apart. The lowest rate was 3.5% in February, which exploded to 14.8% in April. The country lost over 9 million jobs last year, which is a little more than the number of jobs lost in the GFC. The job losses were very acutely felt in the leisure and hospitality industries as travel was restricted. Since then, we have seen cities and businesses reopen. Workers are starting to go back to offices and places of business as they feel safer performing in a socially distant work environment and seek to get out of the monotony of their homes. COVID fatigue has also brought consumers back out and into restaurants and stores. Stimulus checks received thus far, and an even greater stimulus package under the Biden administration should continue to support the recovery. Furthermore, three approved vaccines with more in the pipeline, point to a light at the end of the tunnel. We recognize that the path to recovery will not be smooth and the large strides made thus far will slow its rate of improvement, but as we return to a period of normalcy, pent-up consumer demand should continue to drive longer-term economic growth.

Improving Consumer Behaviors

Source: JPMorgan

On the notably positive side, home sales and housing starts have been strong as people fled the cities for greener, more distanced pastures. The fall in interest rates has supported home-buying with lower mortgage rates. For those who aren’t moving, there has been a notable pickup in spending on home improvement and furnishings as people spend more time in their residences, cooking, working, and working out.

The US is making strides towards a recovery, but it is worth noting that Asia was more proactive in its response to the pandemic and is now on a quicker pace to economic recovery. This can partially be due to the region being more acclimated to viral outbreaks and mask-wearing, as well as certain governments having stronger control over its populations to restrict travel to stifle spread. Nonetheless, growth has reaccelerated in the region and emerging markets will likely further benefit from a coordinated global recovery. Because of this, we are more constructive on the return opportunities of emerging markets, and particularly Asian equities this year.

Operational Leverage May Drive Earnings Outperformance

The pandemic significantly impacted corporate profitability, with an anticipated 11% full year earnings decline for the S&P500 constituents. More defensive sectors, such as Healthcare, Technology, and Staples should end the year with both positive revenue and earnings growth, but cyclical sectors, such as Energy and Industrials are the biggest decliners. While this last year was difficult, the improving economic backdrop during the final quarter should translate into notably improved corporate earnings for the next couple years. More than 80% of the S&P500 constituents have reported fourth quarter earnings so far with the first net positive year-over-year earnings growth since 2019, and the highest growth rate since the same quarter in 2018. On the whole, revenues are recovering, but more notable are the cost reduction efforts during 2020 that have resulted in meaningful margin expansion. Through the recession, companies have reduced fixed costs and overhead where they could to protect what little profits they were able to achieve. We think this belt-tightening can pay off handily for companies into the recovery as costs should rise slower than revenues, resulting in over 20% potential earnings growth on 9% revenue growth. Because of this turnaround in earnings, markets have rallied on appreciation and anticipation for further earnings strength looking forward.

Stocks aren’t Cheap, but Earnings Growth is Strong

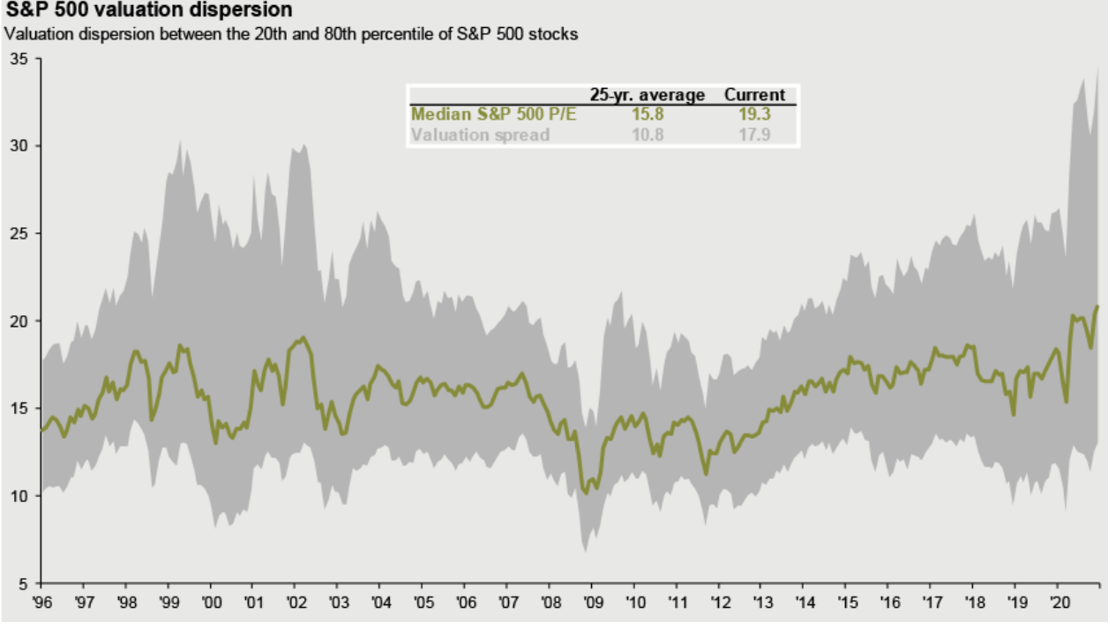

We recognize that stocks seem to be pricing in a lot of the earnings recovery already, with the S&P500 trading at over 22x forward P/E, and meaningfully above historical averages. Cyclical sectors like Consumer Discretionary, Energy, and Tech exhibit the highest multiples, and based on size, small caps are relatively more expensive than their larger peers. These valuations are partially due to strong earnings expectations, but are further backed by the current low-rate environment and monetary policies. The Fed has indicated that it will be very patient before raising rates, and we expect a zero-interest rate policy for the next few years. The Fed is pushing investors into equities by making low-risk assets unappealing from a return perspective, leaving investors with little choice outside of stocks. Earnings growth is a tailwind, while rising inflation will be a headwind. The clash of these factors will create volatility but should still result in returns that outpace bonds and other defensive assets. We do think that small and midcap stocks are best-aligned with the economic and earnings recovery and would thus be overweight, relative to large caps.

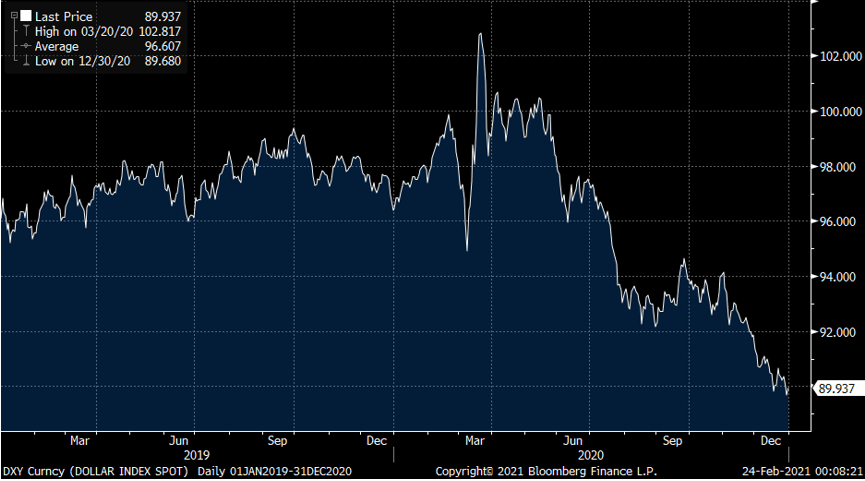

We continue to like the high quality growth opportunity of domestic stocks, but as the dollar weakens and emerging market growth accelerates, we would look to rotate some capital to international equities, particularly in emerging markets and Asia. Up until the recession, the US Dollar was strong, given solid economic growth, and relatively attractive yields on Treasuries. However, as the US cut rates, Treasuries have lost their attraction and the Dollar has weakened. In comparison, emerging market currencies have strengthened along with their economies. This is driving investor interest out of domestic stocks and abroad. Further fiscal stimulus will likely extend this dynamic.

US Dollar Index Spot

Source: JPMorgan

Inflation Headwinds Will Drag on Fixed Income

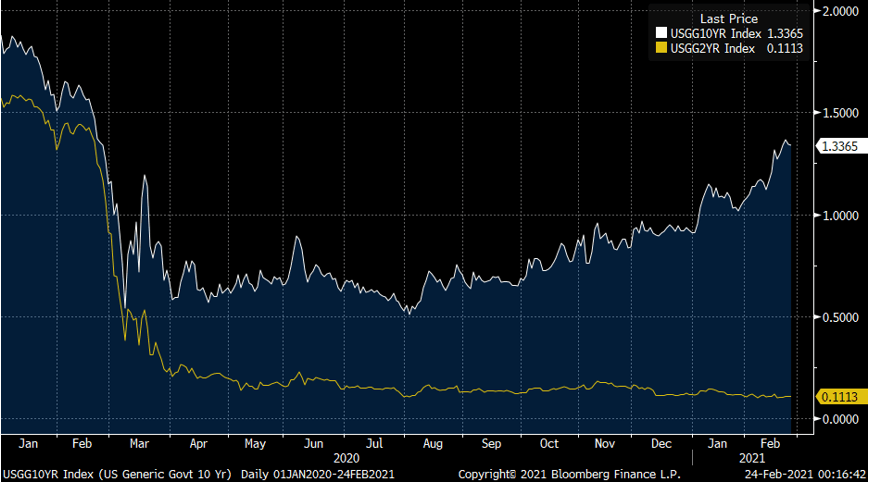

Even though the Fed is targeting a zero-rate environment for the next few years, the markets have been dissenting, pushing 10-year treasuries up over 1.3% from the 0.5% lows from the summer while the two-year note has held at about 0.1%. Very low rates and rising inflation risks make traditional fixed income assets unappealing. We recognize that bonds and stocks are negatively correlated, but the cost of negative real rates make it difficult to own, especially in light of our constructive view on the economy and markets.

Fixed income benefitted in 2019 as well as 2020 from a rate tightening regime, but at current low rates, we would rather own credit-based assets, such as loans and structured credit, than interest-sensitive ones, to collect some nominal yield over inflation. We recognize that liquid spread products are trading relatively tight to historical levels, so we are looking towards structured credit and bespoke lending strategies to enhance return for those looking for income.

Short-term rates haven’t budged. Long-term rates have widened

Source: Bloomberg

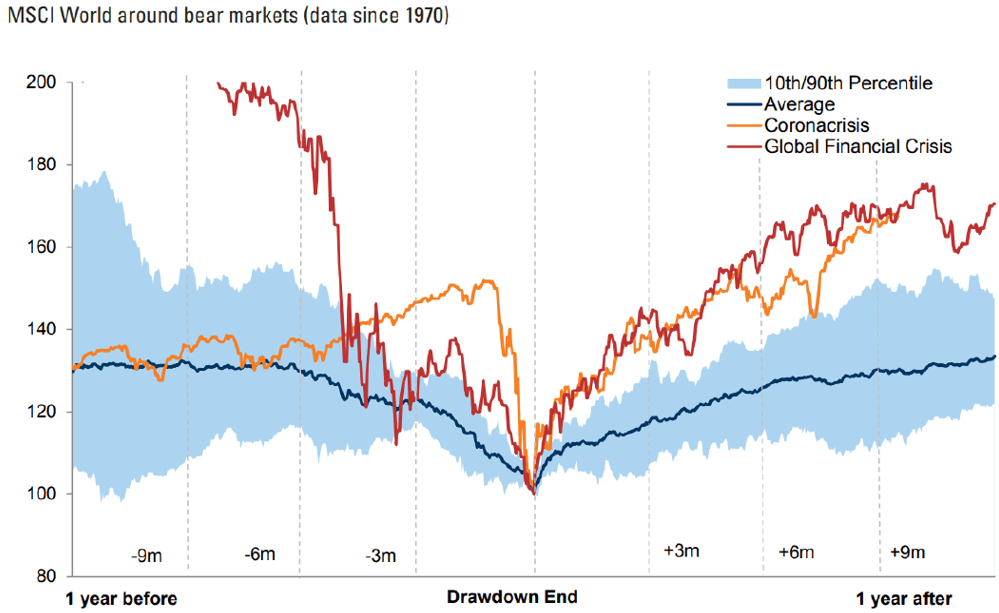

Always Wear Your Seatbelt, but Don’t Expect to Crash

Markets can be very volatile over short periods. The S&P had lost approximately a third of its value through March before closing the year up double-digits in 2020. We anticipate some level of choppiness this year as well, albeit ending solidly positive in the end, as the Fed guides this economy forward.

Source: JPMorgan

Asset Allocation

Equities: Move to Overweight

We remain constructive on equities and are moving our allocation recommendation to a modest overweight as we enter the new year. We recognize that the economy is recovering and the country is adjusting to a new federal administration. Furthermore, it will likely be at least the summer before the world has returned to “normal” with broad inoculations from COVID-19. All the while, domestic social unrest, cyber-incursions from foreign powers, and rebuilding dialogue with international allies on trade and social action will likely make regular appearances in the headlines. Despite these challenges, we are heartened by continued monetary and fiscal stimulus to the economy and capital markets for the foreseeable future. Stimulus will continue, and coupled with low rates and liquidity to backstop markets, the economy should continue to improve. While we haven’t adjusted our growth outlooks higher, we do believe that economic “bear case” risks have been curtailed and we have greater clarity and confidence on the path to recovery. This should continue to push stocks higher and afford a more attractive return opportunity relative to other liquid asset classes.

The market rally has been broader-based in the latest quarter, rather than the preceding leadership of the FAANGs in the middle of 2020. Likewise, while we have maintained our growth orientation in equities, we have shifted the exposure towards small- and mid-cap stocks and are expanding our international equity exposure to take advantage of the cyclical recovery and strengthening of foreign currencies. We have reduced our defensive allocation as election risk is behind us and vaccine distribution will bring the global economy back into expansion.

Fixed Income: Underweight

Low absolute yields and heightened inflationary risks in Fixed income assets generally have caused us to consider this asset class as a source of capital preservation and risk mitigant to equity volatility, rather than being a source of returns. We are underweight the asset class in order to allocate more to public and private equities, and would continue that rotation in periods of unexpected market shocks. The exposure we do maintain in this asset class tends to be in structured credit opportunities that haven’t recovered as quickly as traditional bonds and thus still afford attractive yields. For tax-sensitive investors, municipal bonds, particularly in high yield, provide an attractive relative value opportunity versus comparably rated taxable instruments. This will be furthered by continued federal stimulus and support, and the recovering economy.

Liquid Alternatives: Move to Underweight

We are reducing our recommendation to Liquid Alternatives to underweight as we shift the focus of this asset class towards equity long/short funds and reduce arbitrage and credit-oriented strategies as the economy and markets heal. We remain sanguine on systematic strategies, which have lagged the 2020 rally, but should recover as markets normalize, as well as themes in smaller cap growth, technology, and biotech. We would look to reduce distressed credit exposure as the opportunity hasn’t availed itself to the degree we initially had anticipated.

Illiquid Alternatives: Overweight

We remain overweight illiquid alternatives given their longer investment periods and ability to extract value through active engagement with their portfolio companies. Sponsors have largely been supportive of their companies during the crisis and encouraged them to access liquidity to bridge shortfalls during that period. Additionally, sponsor-backed companies have been opportunistic buyers of weaker businesses during the crisis, which should help them come out of the recession with stronger, more diversified businesses. While an economic recession may impact private business valuations along with their public peers in the short-term, the control held by our managers in executing on operational change and revenue growth can drive true fundamental value creation during the long-term holding periods. Private equity funds will likely experience two to three presidential elections through their fund life, and thus should be considered based on the strategy’s long-term fundamental merits, rather than the current political tone. Over an investment cycle, private equity investments should generate materially stronger returns over public markets in exchange for longer holding periods. We recommend allocations to innovative credit lending, middle-market buy-out, growth equity, and venture opportunities. We currently have a robust pipeline of growth equity and venture capital fundraises coming to market this quarter.

Important Disclosures

This information is for general and educational purposes only. You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from Simon Quick Advisors & Co., LLC (“Simon Quick”) nor should this be construed as an offer to sell or the solicitation of an offer to purchase an interest in a security or separate accounts of any type. Asset Allocation and diversifying asset classes may be used in an effort to manage risk and enhance returns. It does not, however, guarantee a profit or protect against loss. Investing in Liquid and Illiquid Alternative Investments may not be suitable for all investors and involves a high degree of risk. Many Alternative Investments are highly illiquid, meaning that you may not be able to sell your investment when you wish. Risk of Alternative Investments can vary based on the underlying strategies used.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Simon Quick), or any non-investment related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Simon Quick is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. If you are a Simon Quick client, please remember to contact Simon Quick, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services. Simon Quick Advisors, LLC (Simon Quick) is an SEC registered investment adviser with a principal place of business in Morristown, NJ. Simon Quick may only transact business in states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. A copy of our written disclosure brochure discussing our advisory services and fees is available upon request. References to Simon Quick as being “registered” does not imply a certain level of education or expertise.

This newsletter and the accompanying discussion include forward-looking statements. All statements that are not historical facts are forward-looking statements, including any statements that relate to future market conditions, results, operations, strategies or other future conditions or developments and any statements regarding objectives, opportunities, positioning or prospects. Forward-looking statements are necessarily based upon speculation, expectations, estimates and assumptions that are inherently unreliable and subject to significant business, economic and competitive uncertainties and contingencies. Forward-looking statements are not a promise or guaranty about future events.

Economic, index, and performance information herein has been obtained from various third party sources. While we believe the source to be accurate and reliable, Simon Quick has not independently verified the accuracy of information. In addition, Simon Quick makes no representations or warranties with respect to the accuracy, reliability, or utility of information obtained from third parties.

Historical performance results for investment indices and/or categories have been provided for general comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your account holdings correspond directly to any comparative indices or benchmark index, as comparative indices or benchmark index may be more or less volatile than your account holdings. You cannot invest directly in an index.

Indices included in this report are for purposes of comparing your returns to the returns on a broad-based index of securities most comparable to the types of securities held in your account(s). Although your account(s) invest in securities that are generally similar in type to the related indices, the particular issuers, industry segments, geographic regions, and weighting of investments in your account do not necessarily track the index. The indices assume reinvestment of dividends and do not reflect deduction of any fees or expenses.

Please note: Indices are frequently updated and the returns on any given day may differ from those presented in this document. Index data and other information contained herein is supplied from various sources and is believed to be accurate but Simon Quick has not independently verified the accuracy of this information.