Let’s Meet, on Your Terms

No pressure, no obligations — just an open conversation about your goals.

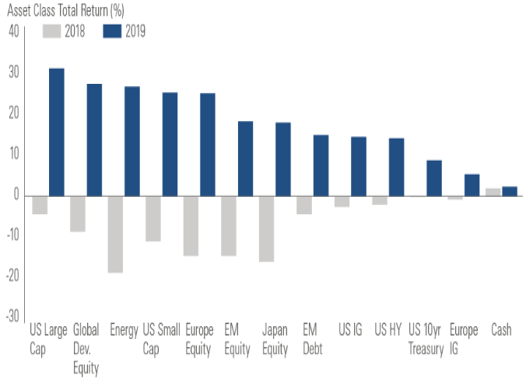

There was a lot to be grateful for over the holidays. Strong investment performance is secondary to health, family, and friends, but it does give one peace of mind to fully enjoy the season. Equity markets marched up over 27% through the first eleven months of the year, with Santa delivering another 3% in December to cap the S&P500 at over 31% for 2019. This was in stark contrast to the coal-in-your-stockings December of 2018 where markets gave up 9% and stood at the precipice of the first bear market since the Global Financial Crisis a decade ago. Stocks weren’t the only ones invited to the party. Fixed income assets also received a healthy bid, with the Barclays Agg returning 8.7% in the year. This was the best performance for the index since the dot-com bubble. International markets and smaller caps also generated strong returns, but domestic equities, particularly growth stocks, were once again the ones everyone wanted to get under the mistletoe.

Source: Goldman Sachs

If you recall, 2017 was a strong year for domestic equities as well, with the S&P500 returning over 20%. But I would argue that it was easier to make money that year than it was this past year. Two years ago, the riskier the asset, the stronger the return, with growth stocks, small caps, international and emerging markets surpassing domestic large caps. In fixed income, high yield bonds outpaced investment grade. The Volatility Index was low, staying in the high single digits for most of the year, barring a few days of spikes where threats of attack from North Korea made the headlines.

In contrast, riskier assets didn’t necessarily outperform in 2019, rather market leaders, those companies with dominant market share and perceived economic cycle resilience, were more likely to do so. The more cyclically sensitive, under-valued stocks, which should typically benefit from a reaccelerating economy, lagged. So why was that? Because if you read the headlines alone on Bloomberg or in the Wall Street Journal, it wouldn’t seem like last year should have been as prosperous as it had been. Recalling some of the fourth quarter highlights:

- Trade tensions between the US and China remained high;

- Corporate earnings were lower year-over-year, with capital investment and manufacturing also on the decline;

- The Federal Reserve lowered rates three times

- The overnight lending market came under stress requiring an injection of liquidity into to the system

- WeWork pulled its $47 billion IPO and then was re-rated down to about $5 billion

- The President of the United States was getting impeached

- The United Kingdom held another general election which sealed the fate for a 2020 Brexit

Our takeaway was that there was still an undertone of trepidation by investors that caused them to gravitate towards large, domestically oriented, asset-light companies, which could arguably be less risky than manufacturing and industrial companies and better-insulated from business cycles than banks. In bonds, interest-rate-sensitive instruments performed better than credit-sensitive ones as Triple-Cs lagged. Investors were willing to buy up-in-quality to be more protective than seeking riskier return opportunities, for most of the year.

We’re now in a new decade, and January brought with it a lot of news. The US and China signed Phase 1 of their trade deal. USMCA (aka NAFTA v2) was also signed the same week impeachment proceedings began in the Senate, particularly notable given it’s an election year. Globally, military tensions escalated for about a week after the US killed Iranian general Qasem Soleimani and braced for retaliation. The deadly coronavirus from China has made its presence known in the US through eleven confirmed cases (at the time of this writing), with the likelihood of more international occurrences before it is controlled. Investors have been walking the tight rope between being too cautious and missing the tremendous performance of recent years, and chasing returns irrespective of equity valuations and the uncertainty around continued earnings growth.

As we mentioned around this time last year, one must invest with a long-term plan that cuts through short-lived volatility and maintain discipline to remain invested for when others are fearful. While that comment was made on the back of a large sell-off in equities, the same applies after strong returning periods as well. We won’t embarrass ourselves by predicting where markets will close at the end of 2020, but we bet anyone that you will rest easy over the long term if you stick to the script of maintaining a well-balanced portfolio regardless of when you’re investing in the business cycle.

Who Won Phase One?

After nearly two years of acrimony between the US and China on a trade deal, with on-again-off-again negotiations whipping around markets, we are now at a détente for the time being. So, what was actually achieved? The US got about $200 billion in additional goods and services to be purchased from China over the next two years. Furthermore, China is expected to strengthen intellectual property protections and potentially pull back on technology transfer requirements from foreign companies. US financial services companies will also have improved opportunities to penetrate Chinese markets with their products. In return, the US partially rolled back its recent tariff increases on $120 billion of imported Chinese goods, but retained its 25% tariffs on $250 billion of goods named earlier that will serve as a bargaining chip for Phase 2 discussions.

Sounds like the US won, but let’s remember, tariffs are paid by the importers, meaning domestic companies, not the foreign supplier, so the still enforced tariffs are being born domestically. Also, the reacceleration of purchases of agricultural goods by China is positive, but will only start a healing process for American farmers rather than being a big financial boon for them when compared to the levels of business previously attained a few years ago. Chinese growth has been slowing, partly due to the trade war, but also as the country naturally matures. Additionally, the financial system is highly leveraged as the government backs many of its state-owned businesses, with questionable sustainability. We should be careful how we expand the presence of our financial sophistication into a somewhat stretched economy. Finally, both parties can exit the deal rather than being forced to abide by its terms.

The punchline…the US won, but not without scars. And there will be a rematch at some point in the future. The clear winner though, were US investors who saw stocks rally on the agreement followed by increased optimism for growth.

Source: Deutsche Bank

Impervious to War and Disease

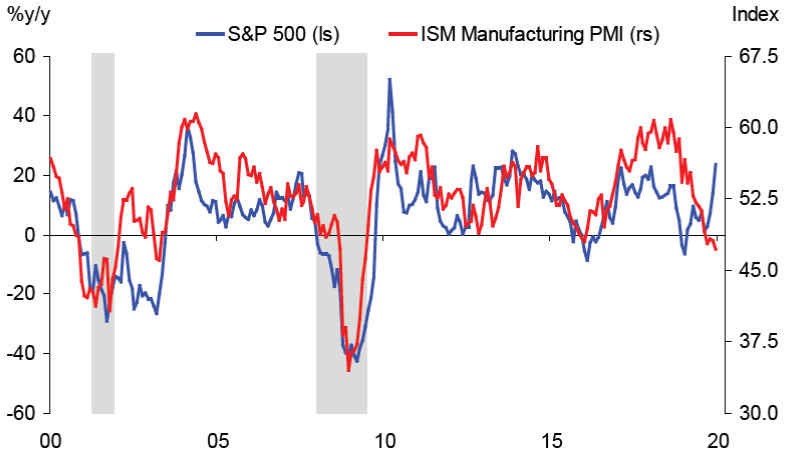

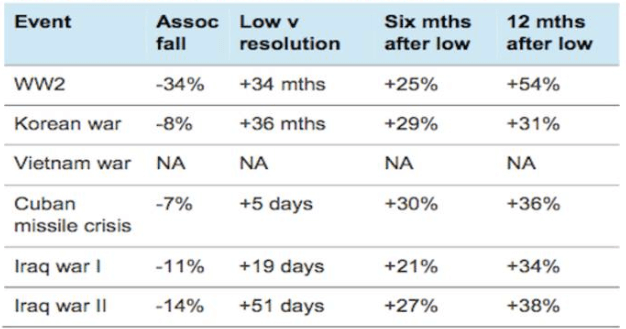

Economic uncertainty and opaque monetary policy are like kryptonite to the markets. However, wars and diseases bounce off the market like bullets off Superman. As soon as we entered the new year, tensions escalated quickly in the Middle East, after the US killed Iranian general Qasem Soleimani in a drone strike. Iran promised retribution and memes popped up all over the internet over how American teens were going to be drafted to fight in World War III. From a markets perspective, equity indices hesitated for a couple days, bracing for the uncertainty of what’s next, but quickly returned to normal. As it turns out, markets may retreat during military escalation, but upon the formal declaration of war, it tends to recover quickly and interestingly outperforms more benign periods.

“A compelling argument for why that is is that wars tend to increase government spending, resulting in increased revenue and earnings for those companies that are awarded government contracts. Wars also entail spending on rebuilding.”

Even more interesting is that volatility actually comes down in periods of war. We saw this in World War II, the Korean War, the Vietnam War, and first Gulf War where large cap stocks were one-third less volatile than the average experience. Also, fixed income instruments, usually a safe haven for capital in periods of uncertainty, actually underperform in these events. And why is that? It can be due to government spending leading to spikes in inflation, resulting in rising interest rates and falling bond prices, exactly the opposite of what you want when looking for protection. This is a very broad characterization, and we recognize our economy has shifted towards the services sector and away from manufacturing, which will have its own unique effects, but this is generally a good rule of thumb for when military sparks flare up. Outbreaks of infectious diseases seem to have the same (lack of) effect. Looking at prior experiences, such as Zika, Ebola, and SARS, markets remain very resilient and generate strong returns within a few months of the outbreak and the bout of volatility would be attractive entry points for tactical trades. We mention this as the coronavirus is spreading in China and is now on our shores. We want everyone to stay safe, but also know that your portfolios will be “ok”.

Source: AMP Capital

Research Spotlight: Going Green

We’re not referring to our fancy new color scheme, rather commenting on “ESG” and impact investing opportunities available here at Simon Quick. A new year’s resolution for these quarterly newsletters is to highlight certain investment ideas we’re working on or have approved on our platform that may be of interest and worth discussing with your client advisor. “ESG” refers to the recognition and motivation to support environmental, social, and governance issues as part of doing business, beyond focusing solely on bottom-line. The term is broad and encompasses elements such as improving efficiency and reducing corporate carbon footprints, gender pay and representation equality, and incentive alignment of management with shareholders, to name a few. “Impact investing” incorporates elements of ESG as a starting point which companies seek to create a positive impact on society as a core goal of being in business, not just seeking to avoid the negative effects. The investment thesis is that companies with good ESG practices can also enhance the bottom-line and thus, doing well (for shareholders) while doing good (for all stakeholders).

TIME’s 2019 Person of the Year is a teenage climate activist named Greta Thunberg who has been pushing adults to consider their impact on the planet and do something to fix it. She spoke at the United General Assembly at the World Economic Forum in Davos. While we don’t currently have any delusion of grandeur in presenting at these future gatherings, we have investigated, diligenced, and approved managers across investment strategies that employ ESG into their investment philosophy, while maintaining or even enhancing returns beyond their non-ESG peers, which we’ll introduce below.

We recently approved a manager in the lower middle market direct lending space. While the field is crowded in direct lending, what notably stands out about this manager is their focus on environmentally focused companies, including agriculture, renewables and power efficiency. The borrowers can be profitable businesses seeking growth capital, in the form of credit, to fund projects that would deliver a scalable solution that provides positive environmental effects. Examples of this would include military-grade portable air decontamination/purification units, electric power delivery for cargo trucks, and biodigester plants for renewable power. The manager is recognized as a specialist in this area and thus doesn’t compete against all the other generalist lenders. Additionally, as the companies are still in their growth stages, the manager typically extracts higher yields and stock rights to supplement returns.

We had approved a venture capital fund of funds that employs an impact strategy by culling through its list of managers that fit within a renewables, healthcare, education tech, fintech, and collaborative economy themes where the majority of the underlying portfolio companies seek to create positive impact for its consumers and their ecosystem. This has a higher risk, higher return target given its venture capital orientation and can be complementary to other asset classes and venture strategies.

Amongst liquid strategies, we have an equity manager with a core competency in managing index- and factor-based portfolios while generating tax losses that can be utilized elsewhere by the client. This manager can employ ESG, socially responsible, and faith-based screens on client portfolios to exclude investment in companies that fail to satisfy certain criteria while still generating returns and tax losses consistent with the targeted benchmark.

Finally, we have an approved municipal bond manager that employs ESG screening to their investment process where, after passing a credit analysis, undergoes an ESG scoring exercise where bonds can only be purchased if they exceed minimum thresholds. The manager will score across elements such as gender equality, carbon footprint, social benefit, efficiency, amongst others, in order to maintain a robust ESG framework for investment.

These are currently approved opportunities in addition to the continuous diligence our Research team conducts in order to discover attractive investments across assets and strategies. We expect ESG to continuously grow as an area of focus over the long-term and become a normal part of evaluation alongside traditional investment and financial performance analyses.

Asset Allocation

Equity: Modest Underweight

Equities finished the year on a strong note, supported by positive sentiment from a US-China trade deal with the backdrop of stable corporate earnings and macro fundamentals. The domestic economy is doing fine and should continue to grind out growth this year. However, stocks have priced a lot of this growth in already, thus conviction in another year of exceptional returns is lower. As we are closer to the end of the business cycle than we are to the beginning, we expect more frequent bouts of volatility and thus find stocks to carry greater risk. We remain modestly underweight equities and continue to maintain a Value and “Quality” tilt primarily through large cap domestic companies, but also have increased small cap exposure on the margin, given the relative underperformance over the past couple years. Internationally, as trade tensions subsiding and Brexit clarity increasing in Europe, we recommend rotating capital back to international developed and emerging market stocks. With the Fed on pause, the dollar will remain strong but potentially stagnant, which would also favor international companies. We believe this allocation posture allows for us to be offensive and add to our equity exposure if the market were to pull back, due to exogenous factors or general market skittishness.

Fixed Income: Target-weight

Rates are expected to remain low for the year, even if we see a pick-up in growth and inflation. While the return opportunity is limited from bonds, they do serve as a counterbalance to equities and should protect on a stock market sell-off. We have modestly extended duration, but still remain short relative to benchmarks, given the lack of additional yield. We remain selective with credit risk and thus have limited exposure to traditional high yield bonds and loans, and instead have opted for structural and liquidity arbitrage options to enhance returns.

Liquid Alternatives: Overweight

We are constructive on hedge funds in the current investment environment. We remain selective on long/short equity managers broadly as the ability to generate consistent excess returns is very difficult. However, we retain a select group of funds in this strategy that we expect to achieve that high hurdle and can be a substitute to the long-only equity risk. Arbitrage, idiosyncratic credit, and un-correlated asset strategies can generate strong, consistent returns ahead of fixed income and without rate sensitivity in a directionless market. Furthermore, increased market volatility can potentially expand the investment opportunity for these strategies as they have modestly longer liquidity terms versus their long-only peers.

Illiquid Alternatives: Overweight

We are overweight illiquid alternatives given their longer investment periods and ability to extract value through active engagement with their portfolio companies. We recognize that valuations in private equity have also risen, but to a lesser extent in the lower middle market space. Furthermore, institutionalizing operations and strategic acquisitions can improve margins and offset some of the purchase premiums. Over an investment cycle, private equity investments should generate materially stronger returns over public markets in exchange for longer holding periods.

Do you have any questions regarding this content? We would love to chat!

Important Disclosures

This information is for general and educational purposes only. You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from Simon Quick Advisors & Co., LLC (“Simon Quick”) nor should this be construed as an offer to sell or the solicitation of an offer to purchase an interest in a security or separate accounts of any type. Asset Allocation and diversifying asset classes may be used in an effort to manage risk and enhance returns. It does not, however, guarantee a profit or protect against loss. Investing in Liquid and Illiquid Alternative Investments may not be suitable for all investors and involves a high degree of risk. Many Alternative Investments are highly illiquid, meaning that you may not be able to sell your investment when you wish. Risk of Alternative Investments can vary based on the underlying strategies used.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Simon Quick), or any non-investment related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Simon Quick is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. If you are a Simon Quick client, please remember to contact Simon Quick, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services.Simon Quick Advisors, LLC (Simon Quick) is an SEC registered investment adviser with a principal place of business in Morristown, NJ. Simon Quick may only transact business in states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. A copy of our written disclosure brochure discussing our advisory services and fees is available upon request. References to Simon Quick as being “registered” does not imply a certain level of education or expertise.

This newsletter and the accompanying discussion include forward-looking statements. All statements that are not historical facts are forward-looking statements, including any statements that relate to future market conditions, results, operations, strategies or other future conditions or developments and any statements regarding objectives, opportunities, positioning or prospects. Forward-looking statements are necessarily based upon speculation, expectations, estimates and assumptions that are inherently unreliable and subject to significant business, economic and competitive uncertainties and contingencies. Forward-looking statements are not a promise or guaranty about future events.

Economic, index, and performance information herein has been obtained from various third party sources. While we believe the source to be accurate and reliable, Simon Quick has not independently verified the accuracy of information. In addition, Simon Quick makes no representations or warranties with respect to the accuracy, reliability, or utility of information obtained from third parties.

Historical performance results for investment indices and/or categories have been provided for general comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your account holdings correspond directly to any comparative indices or benchmark index, as comparative indices or benchmark index may be more or less volatile than your account holdings. You cannot invest directly in an index.

Indices included in this report are for purposes of comparing your returns to the returns on a broad-based index of securities most comparable to the types of securities held in your account(s). Although your account(s) invest in securities that are generally similar in type to the related indices, the particular issuers, industry segments, geographic regions, and weighting of investments in your account do not necessarily track the index. The indices assume reinvestment of dividends and do not reflect deduction of any fees or expenses.

Please note: Indices are frequently updated and the returns on any given day may differ from those presented in this document. Index data and other information contained herein is supplied from various sources and is believed to be accurate but Simon Quick has not independently verified the accuracy of this information.