Let’s Meet, on Your Terms

No pressure, no obligations — just an open conversation about your goals.

Private credit funds have come under scrutiny recently and are receiving a level of negative coverage that, in our view, has outrun the underlying evidence. Private credit, or direct lending to be more specific, typically refers to loans made to businesses to finance a buyout, acquisition, or other funding need. These transactions are made between a single or small group of lenders and the borrower directly and are thus illiquid instruments, meaning not easily tradable like a publicly listed stock or bond. For that illiquidity, these loans typically offer higher yields than their liquid counterparts. These yields were in the low double-digits as recently as 2024. With the backdrop of attractive returns in a benign credit environment, private credit drew a lot of investor interest and Business Development Companies (“BDCs”) became the investment vehicle of choice to gain access. BDCs were an appealing way to invest due to their lower investment minimums, immediate capital deployment, and the possibility of liquidity on a periodic basis. These vehicles provided high-net-worth investors with a way to access an asset class typically reserved for institutions.

Concerns in the asset class started to increase more recently as a few companies came under credit strain and defaulted on their loans. The press took these events as the catalyst for a large default cycle in the space. At the same time, the funds’ double-digit yields declined as interest rates came down. More recently, a notable area of concern has been private credit’s exposure to the software sector, which is facing an identity crisis due to the expansion of artificial intelligence in our personal and professional lives. The confluence of these trends has led investors to look to exit these funds despite an environment of spread widening with limited defaults, resulting in redemption requests in excess of the funds’ typical quarterly limits. Nonetheless, while the natural reaction to reduce exposure in response to negative headlines is understandable, we believe burning down the house to eliminate a few “cockroaches” is not a sound investment strategy.

Let’s consider the role that private credit plays in a portfolio. The asset class delivers a higher return over traditional credit strategies as investors are compensated for the illiquidity and higher risk profile; these are senior secured loans, but to generally smaller, more indebted businesses. This has historically resulted in 2-3% excess return versus liquid leveraged loans and 6% versus traditional investment grade bonds[1]. That premium, when captured by disciplined lenders with strong underwriting and access to deals, should generate attractive long-term returns. Starting in late 2024, narrower spreads and lower base rates began raising questions about the relative value of private credit. While the premium to traditional credit remains positive, it has decreased.

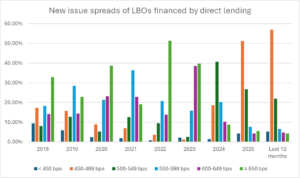

Investors had previously been compensated for incremental risk in private credit, but as the Fed began to cut rates in late 2024, the floating-rate tailwind that had driven investor demand into private credit reversed. In addition to lower base rates, direct lenders must contend with increased competition among their peers and from a recovering broadly syndicated loan market. Increased competition among lenders has meant that spreads on middle-market direct loans declined from over 6% to under 5% since 2024[2]. Yields on direct lending funds have declined by almost 2% since 2024 to around 9% all-in today[3].

While return expectations are coming down in this environment, the fundamental performance of private credit has remained largely intact. Headlines around private credit losses and defaults have been real but relatively modest, and in many cases inaccurately attributed to direct lending specifically. Pluralsight was the market’s first test in 2024 and was broadly absorbed without systemic consequence. Additional defaults came in 2025, such as Tricolor and First Brands, followed by Market Financial Solutions in early 2026. High quality private credit managers largely avoided all these situations while the most significant losses fell on banks, broadly syndicated lenders, and public structured credit vehicles, not the direct lenders.

Despite a recent uptick in credit events in leveraged loans, private credit managers are still seeing stable borrower fundamentals, underscoring the importance of distinguishing pockets of weakness from systemic risk. The rate of defaults has remained consistent with historical levels of 3.5%[4]. Non-accruals, where borrowers haven’t been able to make interest payments, in the asset class were 1.2% of cost at the end of 2025, below the 1.9% average[5]. Direct lending has also historically delivered recovery rates of around 75%, higher than the liquid market, but we do recognize that the gap has compressed more recently[6]. At the same time, interest coverage ratios have actually increased since 2024, driven by lower interest rates that better allow companies to maintain payments. In this current quarter of volatility, spreads have widened 50-100bps from their tights; this will result in some mark-to-market pressure on fund performance but is modest and manageable through income generation[7].

Source: Pitchbook LCD (through 02/28/2026)

Further to this point, we expect higher yields to protect values and support long-term portfolio returns through cycles, even in periods of economic slowdowns. What does feel uncomfortable for private credit is the disruptive impact AI may have on the businesses of the underlying borrowers, specifically within the software sector, which could be about a quarter of lender portfolios[8]. Historically, software businesses have exhibited sticky revenues and large profit margins, making them attractive borrower candidates to lenders. However, AI puts to test the true stickiness of their client base and their willingness to pay for a large contract for something new AI tools can accomplish at a much lower cost.

A wave of generative AI releases triggered a sharp selloff across software and IT stocks and the overall sector fell approximately 30% starting in October 2025. We view AI as an opportunity and threat to many businesses but do not believe it can all be painted with one brush. There will definitively be evolvers and growers, while new AI-driven entrants threaten companies with weaker moats and commoditized products. We recognize there is AI risk in private credit, but the size of the risk is much smaller than what the headlines describe and disruption will play out over a few years. We estimate that of direct lenders’ software exposures, the majority of the loans are with businesses viewed as industry leaders in mission-critical software that is deeply integrated into their customer base and better insulated. Of the remaining exposure, roughly half have the capacity to evolve and take advantage of AI integration, and the other half are at more significant risk. We don’t think the transition will happen immediately but will occur over the next few years. Overall, that means direct lenders’ exposure to AI disruption risk is really in the single digits and overall manageable for direct lenders.

Recent redemption requests have ranged about 2-3 times the fund-level gates of 5%, with investors receiving half or more of their submitted tender requests. Private credit is an illiquid asset, and we don’t want managers to sell loans in the midst of panic, especially when fundamentals remain stable. We believe fund level redemption limits are designed to benefit patient investors as they protect the fund from being a forced seller of assets at uneconomic discounts. While redemption pressures may persist for several quarters before normalizing, we believe the underlying portfolio construction of vehicles allows for stable redemption management. BDCs generate natural liquidity through interest payments and laddered maturities of loans. This organic turnover of up to 20% of the portfolio annually is combined with liquid credit sleeves of 5–10% as an additional line of defense to provide support to the fund to weather through these periods[9].

Overall, we believe the asset class still provides investors with diversification to the private market and incremental income that has been difficult to access outside drawdown vehicles. Headlines and AI-disruption have been driving the narrative, but we believe the fundamentals do not point to a severe default cycle or GFC-type of contagion. Managers that can navigate lower base rates and narrow spreads without stretching into lower quality deals should be able to weather cyclical slowness and generate attractive long-term returns.

We prioritize investing with high-quality managers that have long track records and a history of low losses. These managers have conservative underwriting and are expected to protect against losses. We acknowledge investors will sacrifice some yield for conservative underwriting and high credit quality and believe there is limited additional yield available to those who move to lower credit quality. Position sizing at the onset is important, so investors are not compelled to redeem based on concentration risk in periods of stress. Thus, our fixed income allocation is a balance of liquid investment grade fixed income as well as diversified private credit exposure across direct lending, asset backed lending, structured credit, and other income strategies that can benefit from different risk drivers and diversity of borrower types. That diversified approach is beneficial especially in periods of uncertainty.

Private credit had grown rapidly as it developed into an efficient source of capital for privately held companies and an increasingly attractive source of income for patient, long-term investors. We believe private credit is returning to a more normalized environment and continue to see it as a compelling source of diversified returns as we look forward. We recognize the uncertain environment we’re in today and are readily available to discuss private credit, AI, the Middle East, or any other questions you may have, as it pertains to your portfolios.

Sources

[1] Blackstone. (2026) Private Credit: Fixed Income Performance in Context

[2] Latour, A., & Lakatsky, M. (2024, October 12). Private credit continues to evolve, disrupt the lending landscape. Pitchbook.

[3,5] Sundar, S., & Weiss, A. (2026, March 12). Private credit under the microscope – separating headlines from fundamentals. J.P. Morgan Private Bank.

[4] BlackRock. (2026, February 26). Private credit defaults: the data behind the headlines. BlackRock

[6] Gutner, E. & Herzberg, D. & Yang, R. & Debnath, A. (2025, September 17). Recent middle-market loan recoveries converge with those of large companies. S&P Global

[7] Miller, Z. (2026, March 20). Sea change in private credit delivers long-awaited spread widening. Pitchbook.

[8] Gutner, E. & Palacious, J. & Herzberg, D. & Yang, R. & Parkikh, G. & Averion, C. & Cagampang, C. & Muni, J. (2026, March 17). BDCs’ exposure to software stays high, steady. S&P Global.

[9] Basak, S. & Schwartz, A. & Repetto, P. (2026, March 3). BDC redemptions: looking beyond the gates. iCapital.

Important Disclosures

This information is for general and educational purposes only. You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from Simon Quick Advisors & Co., LLC (“Simon Quick”) nor should this be construed as an offer to sell or the solicitation of an offer to purchase an interest in a security or separate accounts of any type. Asset Allocation and diversifying asset classes may be used in an effort to manage risk and enhance returns. It does not, however, guarantee a profit or protect against loss. Investing in Liquid and Illiquid Alternative Investments may not be suitable for all investors and involves a high degree of risk. Many Alternative Investments are highly illiquid, meaning that you may not be able to sell your investment when you wish. Risk of Alternative Investments can vary based on the underlying strategies used.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Simon Quick), or any non-investment related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Simon Quick is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. If you are a Simon Quick client, please remember to contact Simon Quick, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services.

Simon Quick Advisors, LLC (Simon Quick) is an SEC registered investment adviser with a principal place of business in Morristown, NJ. Simon Quick may only transact business in states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. A copy of our written disclosure brochure discussing our advisory services and fees is available upon request. References to Simon Quick Advisors as being “registered” does not imply a certain level of education or expertise.

This newsletter and the accompanying discussion include forward-looking statements. All statements that are not historical facts are forward-looking statements, including any statements that relate to future market conditions, results, operations, strategies or other future conditions or developments and any statements regarding objectives, opportunities, positioning or prospects. Forward-looking statements are necessarily based upon speculation, expectations, estimates and assumptions that are inherently unreliable and subject to significant business, economic and competitive uncertainties and contingencies. Forward-looking statements are not a promise or guaranty about future events.

Economic, index, and performance information herein has been obtained from various third party sources. While we believe the source to be accurate and reliable, Simon Quick has not independently verified the accuracy of information. In addition, Simon Quick makes no representations or warranties with respect to the accuracy, reliability, or utility of information obtained from third parties.

Historical performance results for investment indices and/or categories have been provided for general comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your account holdings correspond directly to any comparative indices or benchmark index, as comparative indices or benchmark index may be more or less volatile than your account holdings. You cannot invest directly in an index.

Indices included in this report are for purposes of comparing your returns to the returns on a broad-based index of securities most comparable to the types of securities held in your account(s). Although your account(s) invest in securities that are generally similar in type to the related indices, the particular issuers, industry segments, geographic regions, and weighting of investments in your account do not necessarily track the index. The indices assume reinvestment of dividends and do not reflect deduction of any fees or expenses.

Please note: Indices are frequently updated and the returns on any given day may differ from those presented in this document. Index data and other information contained herein is supplied from various sources and is believed to be accurate but Simon Quick has not independently verified the accuracy of this information.