Let’s Meet, on Your Terms

No pressure, no obligations — just an open conversation about your goals.

If you have been keeping an eye on business news this year, odds are you’ve seen the headline “The S&P 500 reaches another record high.” In fact, as of early September, the S&P 500 index has reached a record high 20 times this year. When considering all the events that occurred in 2025, from trade policy to geopolitical events, from the MAG 7 sell-off and rebound to stubbornly high interest rates, corporate America has been quite resilient in the face of a volatile landscape, and investors have benefited.

While the market is currently on pace to have another above-average return for the year, it’s also on track for an above-average year for setting an All-Time High.

Number of all-time highs for the S&P 500 each year

Exhibit A. Frequency of S&P 500: All-Time Highs Occurrences

(S&P 500 historical average for closing at a record high = 18 times per year)

Source: Apolloacademy

With the S&P presently flirting at an All-Time High and a possible third year in a row of double-digit returns, we’ve been asked the question from clients with fresh cash to invest: “Is now the right time to begin buying stocks?” Our response? As any good advisor would say, “It depends on the purpose of this new capital, but one thing you should not do is let the market’s achievement of an “All-Time High” or the concern of a “market sell-off” deter you from investing.

When providing this response to clients, we’ve found the following data points to best illustrate this perspective:

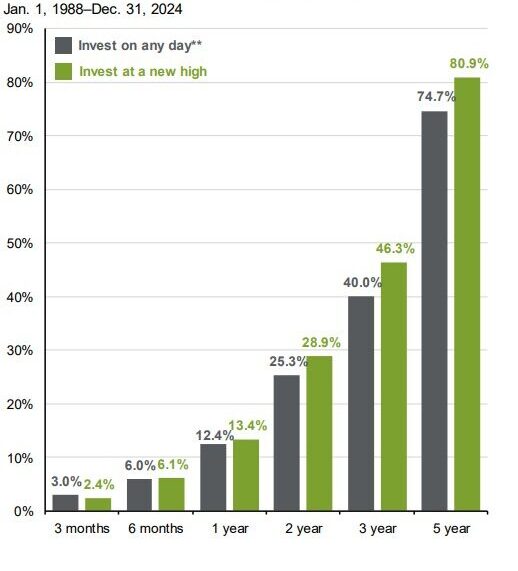

Investing at All-Time Highs can deliver superior returns

On average, investing at an “All-Time High” has actually outperformed investing at “Non All-Time Highs” for holding periods of 6 months and greater.

Average cumulative S&P 500 total returns

Exhibit B. Historical Returns: Investing During All-Time Highs vs. Non All-Time Highs

Source: J.P. Morgan Asset Management

Market corrections after highs are rare

The odds of a material correction (a decline of >10% from the high) are low, as the market has experienced this level of decline in only 9% of time periods one year out and falls significantly when observing the three-year (2%) and five-year time periods (0%).

Exhibit C. Frequency of Market Corrections Following All-Time Highs

Source: Bloomberg, RBC GAM. Data as of January 1, 1950 to March 2024, in U.S. dollars.

Long-term Investors are often rewarded

Over the last ~80 years, if you had invested in the S&P 500 at the start of any calendar year and held that investment for 10 years, you would have experienced a positive rate of return 97% of the time, and on average would have experienced an 11.32% annualized return.

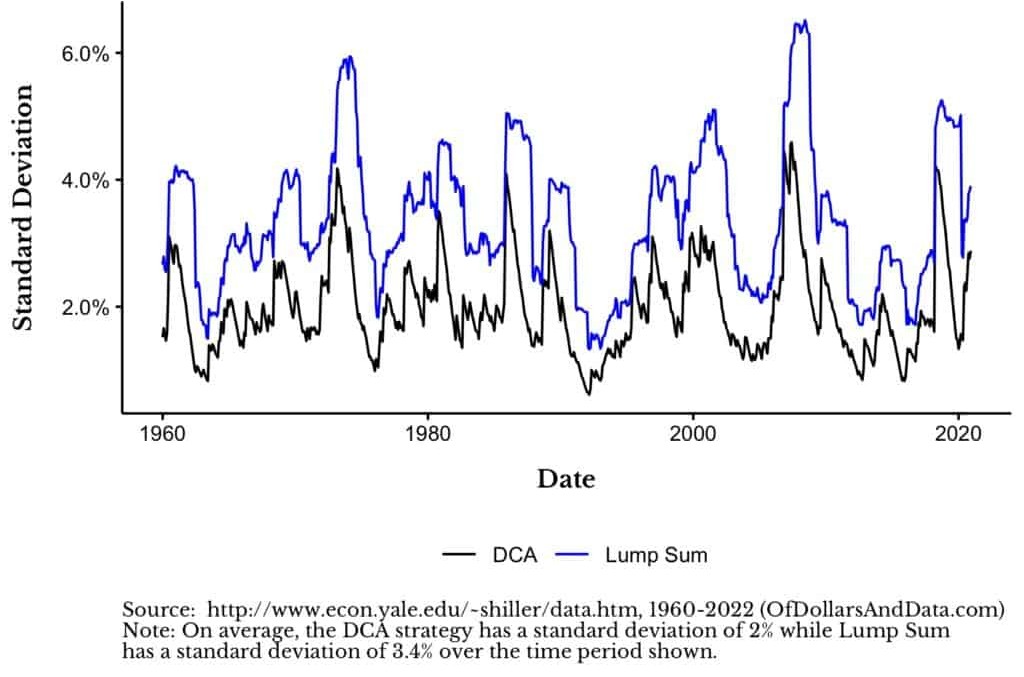

For those with significant risk aversion

For clients who remain risk-averse despite these illustrations, we often discuss Dollar-Cost Averaging (DCA) vs. Lump-Sum (LS) Investment. The data suggest that a DCA approach can mitigate the risk of negative outcomes over shorter time periods (see Exhibit D), when the range of potential returns and the degree of portfolio drawdowns are less extreme. However, DCA also significantly limits upside return potential if you’re investing over longer time periods (see Exhibit E).

Standard deviation for 24-month DCA vs. Lump Sum Investment U.S. Stocks

Exhibit D. 24-month range of return outcomes for LS vs. DCA

Source: Of Dollars And Data

Exhibit E. Ten-Year Compounded Cumulative Return Outcomes

Source: Northwestern Mutual

The Bigger Picture: Timing the market is difficult

In summary, trying to time a market downturn is incredibly difficult; you not only need to know when to sell, but when to buy back in. History has shown that the average equity fund investor often buys in times of market euphoria and sells during times of market panic.

Establishing your investment time horizon for specific buckets of investment capital will allow you to benefit from “time in the market” and not succumb to the temptation of “timing the market”, ultimately helping you avoid costly mistakes and securing positive outcomes with confidence, no matter the market environment or price level.

Disclaimer

This information is for general and educational purposes only. You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from Simon Quick Advisors & Co., LLC (“Simon Quick”) nor should this be construed as an offer to sell or the solicitation of an offer to purchase an interest in a security or separate accounts of any type. Asset Allocation and diversifying asset classes may be used in an effort to manage risk and enhance returns. It does not, however, guarantee a profit or protect against loss. Investing in Liquid and Illiquid Alternative Investments may not be suitable for all investors and involves a high degree of risk. Many Alternative Investments are highly illiquid, meaning that you may not be able to sell your investment when you wish. Risk of Alternative Investments can vary based on the underlying strategies used.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Simon Quick), or any non-investment related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Simon Quick is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. If you are a Simon Quick client, please remember to contact Simon Quick, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services.

Simon Quick Advisors, LLC (Simon Quick) is an SEC registered investment adviser with a principal place of business in Morristown, NJ. Simon Quick may only transact business in states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. A copy of our written disclosure brochure discussing our advisory services and fees is available upon request. References to Simon Quick Advisors as being “registered” does not imply a certain level of education or expertise.

This newsletter and the accompanying discussion include forward-looking statements. All statements that are not historical facts are forward-looking statements, including any statements that relate to future market conditions, results, operations, strategies or other future conditions or developments and any statements regarding objectives, opportunities, positioning or prospects. Forward-looking statements are necessarily based upon speculation, expectations, estimates and assumptions that are inherently unreliable and subject to significant business, economic and competitive uncertainties and contingencies. Forward-looking statements are not a promise or guaranty about future events.

Economic, index, and performance information herein has been obtained from various third party sources. While we believe the source to be accurate and reliable, Simon Quick has not independently verified the accuracy of information. In addition, Simon Quick makes no representations or warranties with respect to the accuracy, reliability, or utility of information obtained from third parties.

Historical performance results for investment indices and/or categories have been provided for general comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your account holdings correspond directly to any comparative indices or benchmark index, as comparative indices or benchmark index may be more or less volatile than your account holdings. You cannot invest directly in an index.

Indices included in this report are for purposes of comparing your returns to the returns on a broad-based index of securities most comparable to the types of securities held in your account(s). Although your account(s) invest in securities that are generally similar in type to the related indices, the particular issuers, industry segments, geographic regions, and weighting of investments in your account do not necessarily track the index. The indices assume reinvestment of dividends and do not reflect deduction of any fees or expenses.

Please note: Indices are frequently updated and the returns on any given day may differ from those presented in this document. Index data and other information contained herein is supplied from various sources and is believed to be accurate but Simon Quick has not independently verified the accuracy of this information.